A New

Year, a New Bull Market?

Many

stock markets have started the year on a tear, with impressive gains seen in

many indices, including the S&P 500 and the FTSE 100 both of which are already

up over 4%.

There are

a number of reasons for this enthusiasm including, a generally rosier view of

the global economy, an increasing belief that global quantitative easing (QE)

will float asset prices higher (triggered by the Bank of Japan’s [BOJ] recent

statement that they intend to print money till their ears bleed, in a final

attempt to kick-start their economy from its 20 year slump), and a continuing

hiatus in the bad news flow emanating from the euro zone. But probably the most

important reason

is the

sense of relief triggered by the ‘resolution’ of the Fiscal Cliff issue.

Heading

into the close of 2012 global investors were concerned about the rumbling

Fiscal Cliff issue, and as a consequence went into ‘risk-off’ mode, meaning

stocks and commodities were sold and the funds reinvested into safe havens like

US Treasury bonds. Compounding this trend were the many pension

funds, investment funds and hedge funds that have the 31st December

as their financial year-end.

Because the

‘bottom line’ of financial institutions dictates the level of bonus payments

that will be made, these institutions tend to become more risk averse the

nearer they get to their end of year date. The last thing they want is to ‘take

a bath’ on the markets when there is little or no time to make the money back,

so they become ‘gun shy’, hanging on to what they have already made rather than

look for more opportunities.

This has

two effects; firstly in periods when there is already a bigger issue

undermining investors’ confidence and the markets are under selling pressure,

this trend is accentuated. And secondly, as soon as the new financial year

begins these same institutions look to redeploy these same funds back into the

market as quickly as possible, leading to a flood of buying and higher prices.

Indeed,

over the last few weeks we have seen some of the biggest flows in to equity

funds since the 2007 peak.

It is the

combination of this rush back into the markets by the financial institutions,

and the sense of relief and optimism and return to ‘risk on’ triggered by the

fiscal cliff deal that is fuelling the current rally.

So will

it continue? Can we look forward to a positive year for stock markets, with an

improving economy and an increased appetite for risk? Or is it just a short

term fillip, soon to wear off?

Lipstick

on a Pig

Although

the last gasp fiscal cliff resolution inspired the confidence of investors, it

was anything but a true resolution. In my last post http://kiwiblackers.blogspot.co.nz/2012/12/the-fiscal-cliff.html

I explained what the fiscal cliff actually was and what I anticipated would

happen, thinking that the most probable outcome would be some partial solution

with the problem being shunted further into the future.

Unsurprisingly

that is pretty much what happened, so in spite of the markets’ vote of

confidence, the problems have not been dealt with or gone away, and have

actually been made worse. But that is a problem for another day it would seem.

We will be hearing much more about both the

fiscal cliff and the debt ceiling in the months ahead.

Back in

the euro zone all has been quiet since the ECB’s announcement back in September

2012 that it would support struggling European countries by unlimited buying of

their short term bonds (in order to keep interest rates down and allow them to

service their debt) via its Outright Monetary Transactions (OMT), leading to a

recovery in many European financial markets.

In the

months following, attention focused on the US as it struggled with its own

debt and solvency issues. However

silence does not equal solution, and although the relative calm may lead us to

believe that blue skies lay ahead for Europe,

it is far more likely that they are actually in the eye of the hurricane.

The

systemic and deep-rooted issues in Europe

remain, and the OMT’s have done nothing to solve the issues, and indeed are not

intended to. But these problems will force themselves to the forefront again

once the ‘juice’ from the OMT’s starts to wear off.

So in

spite of the increased confidence the background picture continues to decay,

with nothing being done to actually resolve the underlying issues, but efforts

focused instead on preventing the system imploding.

Unfortunately all the makeup in the world can’t hide that unpleasant truth.

Unfortunately all the makeup in the world can’t hide that unpleasant truth.

Priced

to Perfection

As we

have discussed in previous posts, markets oscillate around a mean, moving from

overbought to oversold and back again, with extremes of sentiment taking place

at both the major highs and the lows.

At

bottoms investors are very bearish, sick of falling prices and desperate to cut

their losses. As they panic out of their positions, prices collapse leading to

more panic until the market bottoms with a crescendo of selling, and at that

point once everyone that wants to sell has sold and the worst that can happen

has been discounted, only buyers remain and the next rally begins.

At tops it

is the reverse, as prices move up investors become more bullish so more buying

develops pushing prices even higher, this sucks in even more buyers, then as

complacency rules, thoughts of a correction are far from investors minds and

everyone that wants to buy has already bought, at this point all the good news

is discounted, the market is ‘priced to perfection’ and the correction starts.

The

difference is that a bottom is often an event, a few days when sellers

collectively ‘throw in the towel’, and the rally that follows can be fast and

hard creating a ‘V shaped’ bounce. Whereas a top is a process, a series of

rallies and corrections sucking in ever more money and investors often taking

weeks or months and having more of a ‘dome shaped’ appearance.

We can see this in the chart of the S&P 500 index below

It is the manner of this topping process that makes them much harder to identify than bottoms. However there is one useful tool that helps us to track investor sentiment, giving us a way to measure the level of complacency or fear that exists in the stock market.

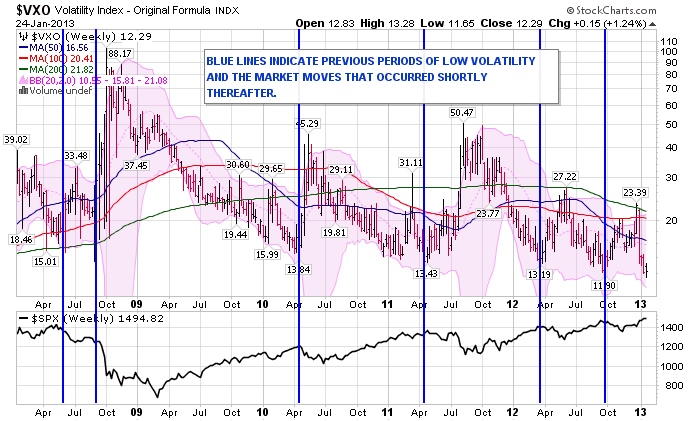

The Fear Index

When funds and large investors

want to lower their risk exposure to the stock market they can of course just

sell some of their holdings, however this isn’t always possible and can

sometimes be prohibitively expensive. Another cheaper solution is to ‘hedge’

your exposure, so that any money you lose on your underlying position is offset

by the money made on your hedge position, giving the same net result as if you

had just sold your underlying.

To achieve this hedge, investors

will often buy ‘put options’ on the S&P 500 index. These options are

derivative contracts that give the buyer the right (but not the obligation) to

sell the index at an agreed price at some point in the future, they therefore

go up in value when the index falls and decrease in price when the index

rallies.

Because you only buy the right to

sell not the obligation, these options are cheap in relation to the level of

protection they offer, so like an insurance policy they protect you when you

need it and when you don’t they are just the price you pay for peace of mind.

It is therefore easy to see that

during periods when investors are bullish and can see no risk to their

portfolios, they do not feel the need to buy put options as a hedge and as a

result these options trade quite cheaply. The converse is true when investors

are bearish, fear is rife, and markets are falling. At these times the demand

for put options explodes, as does the price.

Fortunately for us, there is an

index that tracks this relative pricing of put options known as the CBOE

S&P 100 Volatility Index. It is important to note that there is more than

one volatility index, and that the methodology used to calculate it is far more

complex than I have described, but for our purposes if we visualise high readings

as meaning fear and low readings as complacency, it will suffice.

On the chart below I have added

the price of the S&P 500 index to the volatility chart. We can see that

volatility is currently very low, and that on previous occasions when it was

around this level a stock market correction wasn’t far away.

Conclusion

January is

often a positive month for equities as money is ‘put to work’ in the markets,

but this year that trend is being magnified by the fiscal cliff debacle. We

know that the money flows into equities are the biggest they have been for many

years, a sure sign that ‘Joe Blow’ investor is bullish, and this high level of

complacency is substantiated by the very low levels of fear shown in the

Volatility Index.

When we

add this to the deteriorating background picture and the fact that many equity

markets are close to heavy overhead resistance (as shown in the chart of the

S&P500 Index below), it is hard to see a positive long term outlook, this

is just not the recipe for a new bull market.

Having

said all this, it is crucial to understand that in spite of the overextended

state of the markets, there is nothing to stop them rallying a little further

before the correction begins, as we have already seen these tops can take a

frustratingly long time to complete, but this should be the last gasp of the

cyclical bounce from the 2009 lows.

We just need

to be patient and wait for the markets themselves to tell us when the time is

right, rather than trying to ‘jump the gun’; because as John Maynard Keynes

famously said ‘The market can stay

irrational longer than you can stay solvent’.